seven a way to fix your Yahoo See digital camera if it’s not doing work

- Should your cam actually working in Bing See, take to to find out if it’s in almost every other applications.

- Along with make certain Bing Fulfill has permission to use your camera which Chrome is determined to allow the camera in the See too.

- Here are 7 the simplest way so you’re able to troubleshoot and you will boost the camera when it’s not working from inside the Google Satisfy.

Yahoo Fulfill makes you home based or perform remote meetings with people globally, but in spite of this, the service possibly has its share out-of hiccups.

To start with: If you want to start a call and find that Google Meet’s cam isn’t working. If you attempt to start a conference and acquire there is no films, or you see an error message proving the digital camera actually available, you could generally improve this dilemma on your own.

Ensure the camera try turned on and you may connected

Normally, you are probably having fun with a cam which is included in the product, for example a camera integrated into your own cellular telephone otherwise laptop. In case you additional an external, plug-from inside the webcam on the desktop computer, guarantee that it’s securely linked. Find out that it’s plugged in and you can deals with an excellent some other application. If you use Window, like, simply click Initiate and type „cam.“ Start the digital camera software once you see they from the research abilities, and make sure you can see videos throughout the app’s window. Otherwise, plug they to the yet another USB port otherwise are most other problem solving procedures to have it performing.

Make sure Google Meet have permission to utilize your camera

On a new iphone 4, start the Options software and tap Confidentiality & Coverage. Tap Cam and make certain Satisfy was activated because of the swiping the fresh new key off to the right.

Read More» Posted by Administrator | 0 comments

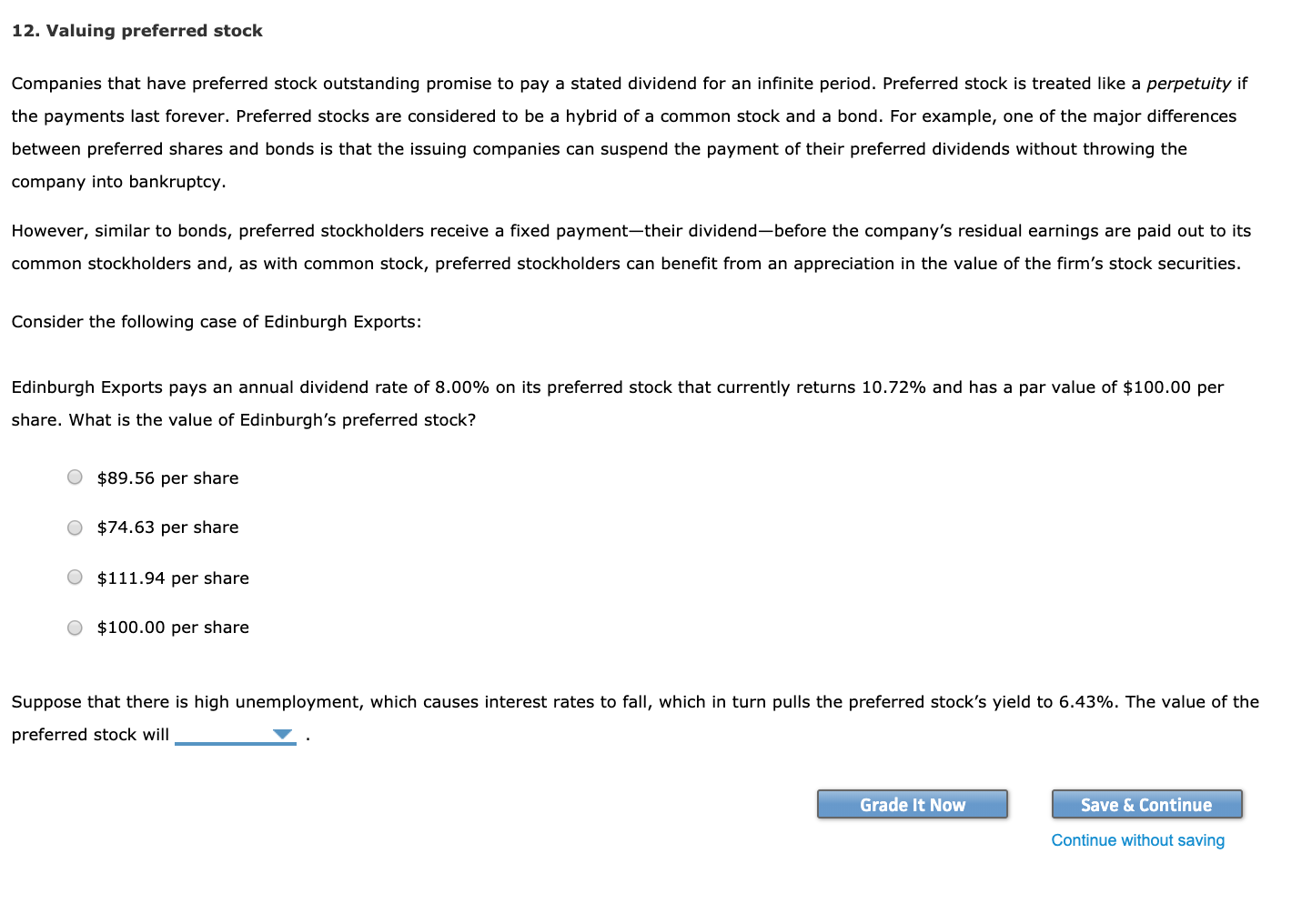

Neueste Kommentare